First time transfer?

Get a special FX rate on your transfer! Send between USD 1 and USD 3,000 today.

What our customers say

Send money from USA to 60+ countries

If you cannot find the location you would like to send to, it means we currently do not support transfers to that destination, but we are working on it! Do come back and check again as we are continuously updating our services.

More currency pairings for USD

If you cannot find your desired currency pair, it means that transfers to that specified currency are not supported by our services, but we are working on it! Do come back and check again as we are continuously updating our services.

Our latest articles

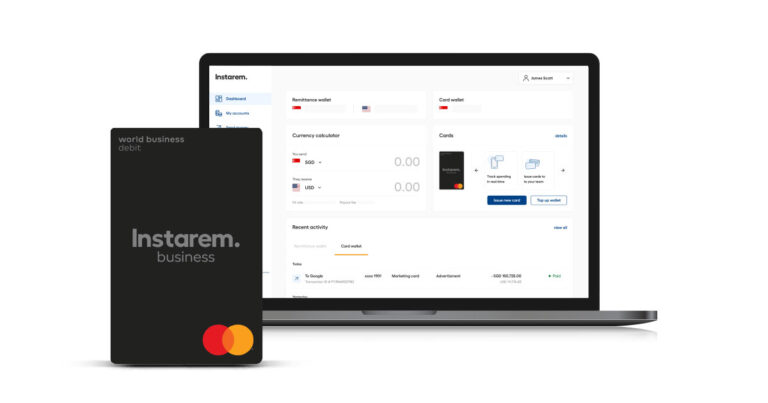

Redefining business expense management with the Instarem Business Card

In today’s fast-moving business landscape, managing expenses with precision and efficiency is no…

Instarem Business Card Security: How to prevent fraud & stay protected

We’re not talking about business name cards here—we’re talking about business bank…

How to transfer a large amount of money with Bendigo Bank in 2025

Sending large amounts of money across borders can be complex, but Bendigo Bank makes it…

How to transfer a large amount of money with Rabobank in 2025

Rabobank Australia makes transferring large sums—both domestically and internationally—simple, secure, and reliable. With…

How to transfer a large amount of money with Bank of Queensland in 2025

Sending large amounts of money across borders can be complex, but Bank of Queensland (BOQ…

How to transfer a large amount of money with Bank First in 2025

Sending large amounts of money across borders can be complex, but Bank First makes it…

From high fees to high touch: How TRUVI transformed global payments with Instarem

The company TRUVI is a premier luxury travel and lifestyle concierge company specializing in personalized…

Average salary in Canada 2025: Industrywise per-hour salary

When you start looking for a new job or role, the average salary offered by…

Average salary in Singapore in 2025 – The ultimate guide

Singapore is one of the most thriving economies in the world. With a booming job…

How to transfer a large amount of money with DBS in 2025

Sending large amounts of money across borders can be complex, but DBS Singapore makes it…