Making your first transfer?

Get a special FX rate on your transfer! Send between USD 1 and USD 3,000 today.

Plus, enjoy USD 5 off your first transfer of USD 1,000 or more. Use code WELCOME.

What our customers say

Send money from USA to 60+ countries

If you cannot find the location you would like to send to, it means we currently do not support transfers to that destination, but we are working on it! Do come back and check again as we are continuously updating our services.

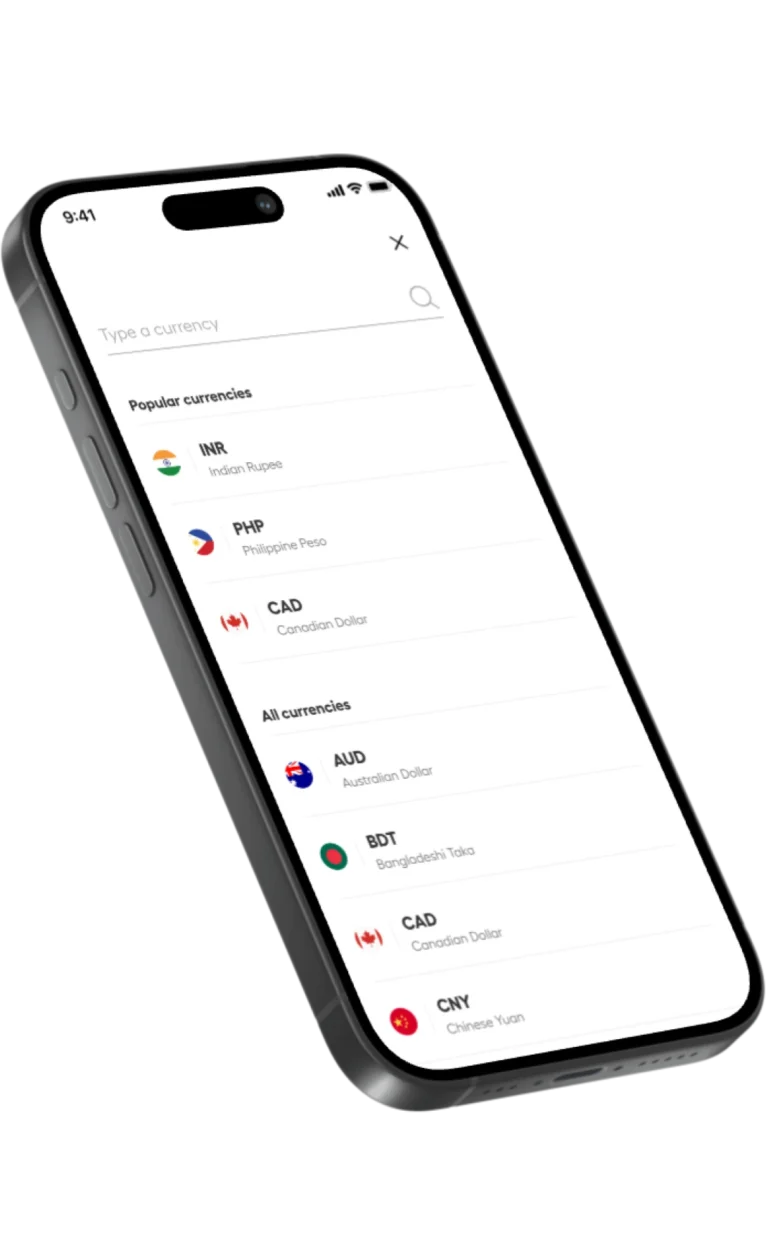

More currency pairings for USD

If you cannot find your desired currency pair, it means that transfers to that specified currency are not supported by our services, but we are working on it! Do come back and check again as we are continuously updating our services.

Our latest articles

Auto top-up is here: Enjoy uninterrupted spending with amaze wallet

You’re next in line. Coffee in one hand, card in the other. You…

Instarem takes home a win at the WeMoney Travel Awards 2026

We’re proud to share that Instarem has been named Best for Flexibility…

FX costs optimisation for BPOs: Reduce losses on global payroll

Key takeaways Acting as third-party partners for businesses looking to streamline operations, BPO (business…

Worker classification for BPOs: Contractor vs employee across APAC (and why it affects how you pay them)

Key takeaways If you run or manage a BPO, you know talent can sit anywhere…

How Hong Kong importers and SMEs can save on every cross-border payment

Key takeaways Running a trade firm in Hong Kong means you send money across the…

Best international business payment platforms in Hong Kong (2026): Banks vs fintech compared

Key takeaways When choosing a platform, businesses should evaluate FX transparency, payment coverage, batch payment…

Best card for online shopping from US, UK & EU sites (For Singaporeans in 2026)

Key takeaways With just a few taps on your phone, you can browse a vintage…

How to earn KrisFlyer miles without a miles credit card: The amaze card way

Key takeaways: Most travel rewards go to people with miles credit cards. The amaze card…

amaze vs YouTrip vs Wise vs Revolut — Best card for SG travellers in 2026

Quick comparison: how travel cards stack up in 2026 Features amaze YouTrip Wise Revolut (Standard…

Scaling payroll operations: FX and fund transfer tips for high-growth tech firms in Singapore

Key takeaways • Global payroll becomes expensive quickly without the right structure. Relying on a single…