UAE Golden Visa from Singapore: Property Rules & How to Transfer Funds Guide (2026)

This article covers:

Key takeaways

- The UAE Golden Visa grants 10-year, self-sponsored residency with no minimum stay requirement, making it viable as a secondary residency for Singapore-based investors.

- The real estate pathway requires a minimum investment of AED 2 million (approximately SGD 735,000 at 2026 rates) in UAE freehold property.

- Traditional Singaporean banks typically apply an FX markup of 1.5%–3% on SGD-to-AED transfers, which on an AED 2 million transaction equates to a loss of SGD 11,000–22,000.

- Instarem is licensed as a Major Payment Institution by the Monetary Authority of Singapore (MAS) and offers rates closer to the mid-market rate for SGD-to-AED transfers.

- Off-plan properties qualify once the buyer has paid the required down payment and received an Oqood certificate — the purchase does not need to be complete.

The United Arab Emirates has rapidly become a premier destination for global investors, highly skilled professionals, and expatriates living in Singapore. With zero personal income tax, world-class infrastructure, and a strategic geographic location, the appeal is undeniable.

For high-net-worth individuals and investors in Singapore, the UAE Golden Visa is the ultimate gateway to this lifestyle. It grants a 10-year, self-sponsored residency, offering unparalleled freedom and long-term stability. The most popular and straightforward pathway to secure it is through real estate investment.

However, purchasing a property overseas comes with a significant, often overlooked hurdle: cross-border capital transfer. Moving millions of Dirhams from Singapore to Dubai via traditional banking can result in massive financial losses due to hidden exchange rate markups.

This guide breaks down the exact 2026 requirements for the UAE Golden Visa via property investment, how to navigate the process, and the smartest, most cost-effective way to transfer your funds from SGD to AED.

What is the UAE Golden Visa?

The UAE Golden Visa is a long-term residence visa issued by the Federal Authority for Identity, Citizenship, Customs & Port Security (ICP). It provides 10-year renewable residency in the UAE without requiring a local employer or sponsor.

Key Benefits of the Golden Visa:

- Valid for 10 years and renewable on the same investment criteria, the visa covers residency across all Emirates, including Dubai and Abu Dhabi.

- Allows the holder to sponsor a spouse, children (unmarried sons under 25, daughters of any age), and domestic staff.

- No minimum stay requirement — holders can maintain primary residency in Singapore without the visa lapsing.

- The UAE imposes no personal income tax, capital gains tax, or wealth tax on individuals.

The Real Estate Pathway: The “AED 2 Million” Rule

The most straightforward Golden Visa pathway for Singapore-based investors is the Real Estate Investor route. The 2026 requirement is a minimum property investment of AED 2 million (approximately SGD 735,000, depending on live exchange rates).

What qualifies:

- Ready (completed) properties — full ownership, title deed issued by the Dubai Land Department (DLD).

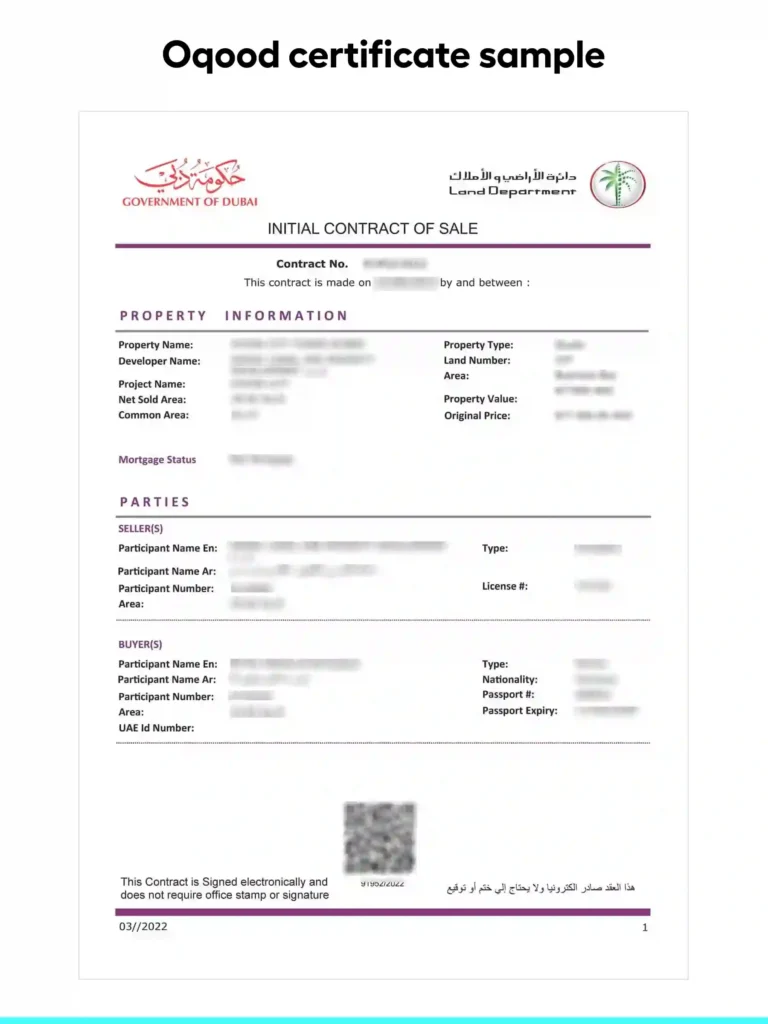

- Off-plan (under construction) properties — qualify once the required down payment is paid and the Oqood certificate is issued. Visa application can begin before construction completes.

- Multiple properties — the AED 2 million threshold can be met by combining the value of several lower-priced units.

- Joint ownership — married couples can co-own a property, provided the combined share equals at least AED 2 million.

- Mortgaged properties: UAE bank financing is permitted. The lender must provide a No Objection Certificate (NOC), and the applicant’s paid equity must meet the minimum threshold set by the ICP.

The Cost of Using a Bank to Transfer SGD to AED

Transferring large sums from Singapore to Dubai via a traditional bank typically involves two costs:

- SWIFT/cable fees — flat transaction charges levied by the sending bank and any intermediary banks.

- FX markup — banks apply a spread above the mid-market exchange rate, typically 1.5% to 3% on SGD-to-AED conversions.

Worked example — AED 2,000,000 property transfer:

| Rate Type | SGD Cost | Additional SGD Paid |

| Mid-market rate | SGD 735,000 | — |

| Bank rate (1.5% markup) | SGD 746,025 | SGD 11,025 |

| Bank rate (3% markup) | SGD 757,050 | SGD 22,050 |

The FX loss is realised before the property transaction even completes. On an investment structured around a 4–6% annual rental yield, a SGD 11,000–22,000 FX loss is equivalent to losing two to four months of rental income before the investor takes ownership.

The 4% Dubai Land Department (DLD) registration fee — a mandatory cost on all Dubai property transactions — is an additional AED transfer, compounding the exposure to poor exchange rates.

How to Transfer SGD to AED: What to Look For

When selecting a provider for large SGD-to-AED transfers, evaluate on these criteria:

- Rate transparency — provider should display the mid-market rate and its own rate side-by-side before you commit.

- No deduction in transit — the exact AED amount should arrive in the recipient’s account; SWIFT intermediary deductions should not apply.

- Regulatory status — for transfers originating in Singapore, the provider should hold a Major Payment Institution (MPI) licence from MAS.

- Escrow compatibility — under UAE law, off-plan property payments must be sent to a developer’s regulated escrow account, not an operational account. Confirm the provider can send directly to an escrow IBAN.

Instarem holds an MPI licence from MAS and offers SGD-to-AED exchange rates close to the mid-market rate. Transfers earn InstaPoints, redeemable against fees on subsequent transactions — useful for recurring payments such as DLD fees, developer instalment plans, or property maintenance charges.

Pro tip: Always request the developer’s escrow account IBAN from your Dubai real estate broker before initiating any transfer. UAE law prohibits off-plan payments to a developer’s general operating account.

Step-by-Step: Securing Your Property and Golden Visa

If you are managing this process from Singapore, here is the roadmap:

Step 1: Select a freehold property

Foreign nationals can own UAE property outright only in designated freehold zones (e.g., Downtown Dubai, Dubai Marina, Business Bay, Palm Jumeirah). Confirm freehold status before paying a booking fee.

Step 2: Pay the booking fee and down payment

Reserve the unit with the developer’s booking fee. Transfer the downpayment and the mandatory 4% DLD registration fee directly to the developer’s escrow account. Use a provider offering rates close to the mid-market SGD to AED rate to avoid FX losses at this stage. Use a provider set up to send money to the UAE from Singapore at near-mid-market rates

Step 3: Obtain the title document

Off-plan: Developer issues an Oqood certificate (registered with the DLD) once the downpayment clears. Ready property: Title Deed issued by the DLD.

Step 4: Submit the Golden Visa application

Applications are submitted through the Dubai Land Department’s “Cube” service centre or the ICP online portal. A UAE-based visa consultant can manage this remotely on your behalf.

Step 5: Complete medical and biometrics in the UAE

One in-person trip to the UAE is required to complete a mandatory medical fitness test and register biometrics for your Emirates ID. Most applicants receive visa approval and their Emirates ID within 2–4 weeks of submitting documentation.

Frequently Asked Questions (FAQs)

Can I use a UAE mortgage and still qualify for the Golden Visa?

Yes — UAE bank financing is permitted, but the bank must issue a No Objection Certificate (NOC) and your paid equity must meet the ICP’s minimum threshold. The full AED 2 million does not need to be unencumbered.

Is it safe to transfer property funds via a digital remittance platform?

Yes, provided the platform holds the appropriate regulatory licence. In Singapore, look for providers licensed as a Major Payment Institution by MAS — these are subject to mandatory AML controls and client fund safeguarding requirements equivalent to those applied to banks.

How long does the Golden Visa application take once the property is purchased?

Most applicants receive visa approval and an Emirates ID within 2–4 weeks of submitting property documents through the DLD or ICP portal.

Can I sell the property after receiving the Golden Visa?

You must retain ownership for a minimum of two years after the visa is issued. Selling within that window without reinvesting in a qualifying asset will affect renewal eligibility.

Ready to Fund Your UAE Property Investment?

Skip the bank queues and hidden exchange rate markups. Sign up with Instarem today and experience faster, cheaper, and more transparent international transfers.

Download the Instarem app now and check live SGD to AED rates